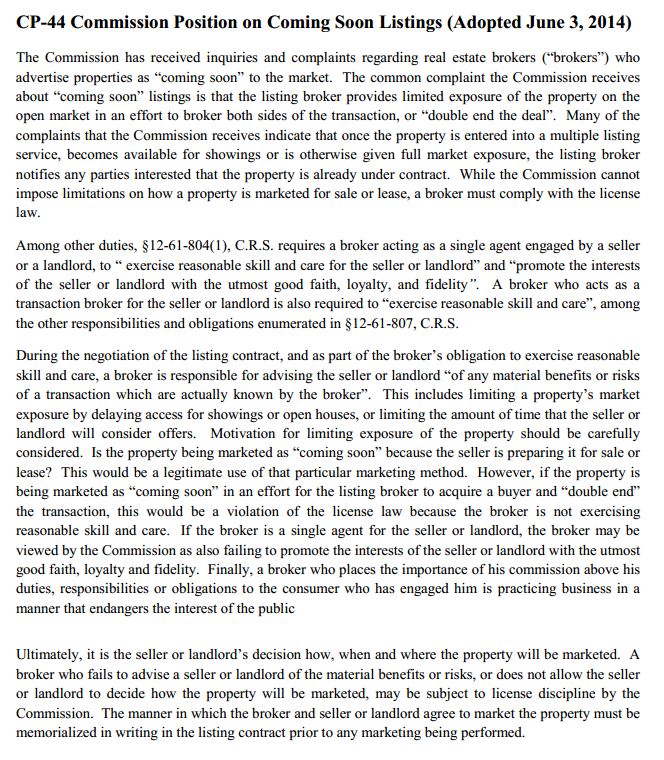

Click the image to read the text of CP-44, Adopted June 3, 2014…  The Colorado Division of Real Estate site is here.

The Colorado Division of Real Estate site is here.

Category: Education

AMC Appraisal Fees and Disclosure- Joshua Walitt

The proposed AMC Rules from the Agencies are out in draft form. Coalitions, industry organizations, and groups of appraisers are examining these and other Rules. There is discussion amongst appraiser groups and other industry participants like never before. It’s a great time to make your voice heard and to hear what others have to say!

When I helped put together a petition to the CFPB a few weeks ago (related to correcting the Customary and Reasonable Fee Rules which allows circumventing the intent of Dodd-Frank), I never imagined the amount of responses I would receive. With so much change going on in the industry, I encourage every appraiser to be involved:

-

What is your Appraiser Coalition doing?

-

How can you be involved in the local chapters of AI and other appraisal organizations?

-

Have you read your State’s Appraiser and AMC rules?

-

Have you read the Appraiser Independence rules established by CFPB, HUD, the Agencies, and other entities?

-

Who do you contact if you have questions regarding State laws and rules?

-

Have you contacted the CFPB regarding enforcement of Appraiser Independence or Customary and Reasonable Fees?

-

Have you completed any and all available fee surveys related to establishing your area’s typical (aka Customary and Reasonable) fees?

-

When was the last time you met with other appraisers in your area?

-

Have you signed and shared the Petition to the CFPB?

-

Are you part of online discussion groups that are positive and share useful information?

Obviously, we all need time to do our work, but issues related to our independence and our fees are part of the foundation of that work itself, so we need to make time to be engaged in the industry discussion. My talk at Valuation Expo this June will touch on related fee issues, with the overall topic being compliance-related issues and their practical applications to our everyday work.

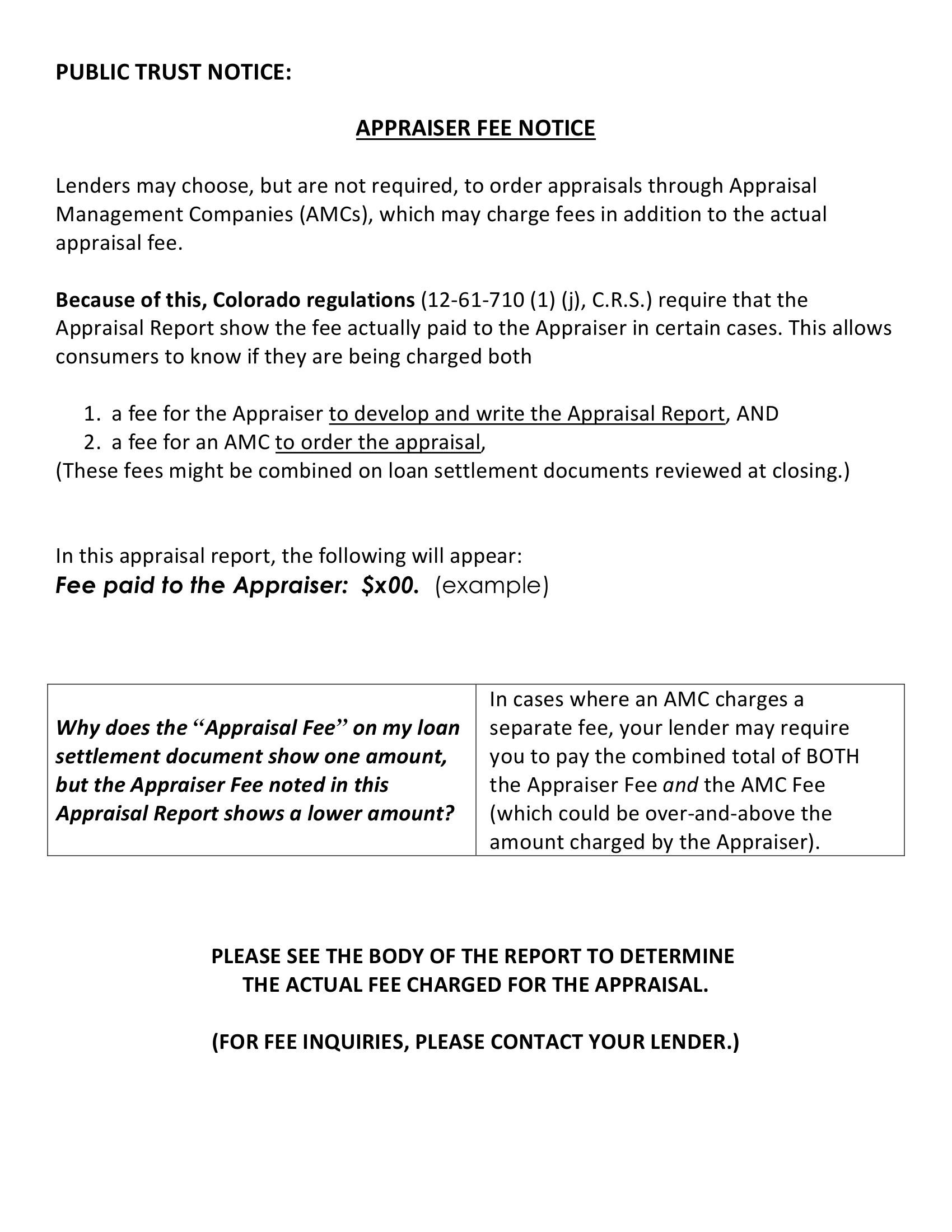

One argument against the Rule-based solution is the assumption that consumers, in the end, really don’t care how much an appraiser is paid. (So is this really a consumer issue? the argument goes.) While consumers may not care about an appraiser’s paycheck per se, let’s not fool ourselves: consumers do care 1) how much they are paying, and 2) what they are paying for. I would argue that consumers DO care how much the appraiser is receiving – since it may differ from what they are charged on the settlement sheet (which may reflect a higher fee than is necessary).

If a loan settlement document shows the consumer is being charged $600 for the Appraisal Fee, I think that consumer would find it surprising – and confusing – to learn the appraiser was actually paid $300 (this is an illustration). Even real estate agents and loan officers tell me they are confused over this issue: Why does the appraisal report say the fee is $300, but the borrower is being charged $600?

The CFPB allows lenders to separate the two fees on the settlement document. But in situations where the lender chooses to comingle the fees on the settlement document, the consumer may not realize they are being required to pay an AMC fee – which is an optional service.

To help alleviate this confusion, many states now require appraisers to post their fees in the reports. HUD also gives this authority to the appraiser for FHA appraisals. (Some AMCs expect the appraiser to post the breakdown of fees within the body of the report.) I have posted my fee in appraisal reports for years.

But be sure to include a disclosure explaining why the Appraisal Fee on settlement documents may differ from the fee you’ve typed in your report, so there is a clear explanation of any “additional” or “different” fees. Take a look at a sample here.

In the end, Appraiser Independence and Fee issues are complex and there is no easy one-route solution. We must proceed with caution.

My two points today:

-

CFPB Rules related to C & R Fees do not allow for any real enforcement of Dodd-Frank, and need correction.

-

Post the Appraiser Fee in the body of the appraisal report with a clear and understandable explanation to avoid consumers misundertanding settlement documents.

Take a look at the Petition, and please sign and share it. But don’t stop there: Know your industry, Get involved, Take action.

Josh Walitt

Originally published at appraisalbuzz.com .

Appraiser Fee Disclosure sample

Here’s the sample Appraiser Fee Disclosure. (Click the image.)

Q & A with Josh Walitt on Residential Appraisals Colorado

Question #1:

Question #1:

My bank said they ordered an appraisal for my loan, but no one ever came inside the house. Does this sound right to you?

For certain types of loans, such as home equity loans, banks follow specific federal guidelines (called Interagency Guidelines) which allow for the bank to use an exterior-only appraisal from a licensed or certified appraiser in some cases. These types of exterior appraisals are typically used in low-risk lending situations, and can also used by banks for pre-foreclosure, loss-mitigation, and similar situations. Since the property is only observed from the street, the homeowner may not even know that the appraiser’s visit took place.

With exterior-only appraisals (sometimes referred to as “drive-bys”), assumptions are made about the interior, sides (if not visible from the street), and rear of the property, as well as the site in general, based on the limited viewing of the property, along with public records, any records in the local real estate MLS system, aerial imagery, or file information the appraiser has on the property, as long as the sources are determined to be reliable. For example, the appraiser may see that the visible parts of the property are in average condition displaying little-to-no needed repairs, so he could assume that the entire property is of similar condition. Or, based on the county records, the appraiser could assume the subject has a covered back patio, a fireplace, and a detached utility building, none of which is visible from the street. Keep in mind, these exterior-only appraisals are not typically ordered for first-mortgage loans, such as when you buy a house.

For first mortgages, a full appraisal is usually conducted, which includes the appraiser viewing the inside and outside of the property. In these situations, the inventory of the property is observed by the appraiser (rather than making assumptions, as in exterior reports). However, it is important to remember that the appraiser is not a home inspector, so he will still make certain assumptions. For example, the appraiser may assume the utilities are functional, the structure is sound, there are no health hazards, and so on, as long as there is no evidence to the contrary.

There are some situations where the bank can loan without the use of an appraisal. If there is ever any question, remember this: a borrower can ask to review copies of all valuation reports that the lender used.

Question #2:

I got my own appraisal a few months ago because I was thinking of listing my house for sale. Now I want to refinance, but my banker won’t take that appraisal.

There are several factors at work here.

First, banks are required to order their own appraisals, ensuring certain Appraiser Independence regulations are met. For a privately ordered appraisal, such as for a legal matter, a trust, an estate following a death, or a pre-listing appraisal, these regulatory safeguards are most likely not met. Banks and lenders have internal departments and staff that carry out and monitor the appraisal-ordering procedures, although some choose to use third parties.

Second, an appraisal has specified Intended Use and Intended Users. To follow federal rule, appraisers must identify the Use and Users of an appraisal report. Examples include: to determine a property’s market value to aid in listing it for sale by the homeowner and real estate agent, to determine market value for divorce purposes by Mr. Smith and his attorney, and so on. The Use and User for lending appraisals may often be to evaluate the property for mortgage purposes by the lender.

Why is this so important? The Use can impact what the appraiser is trying to solve: is it liquidation value, market value, a range of values, before- and after- remodel values, a future anticipated sale price? And the Intended User can be a very important factor in the level of detail and information that the appraiser provides in his report. For example, writing for a lender, the appraiser would not hesitate to use terms such as “bracketing”, “highest-and-best use”, “super-adequacy”, “regression analysis”, and so on; these terms could confuse many homeowners, agents, or attorneys, unless there was further explanation in the report. Consider that the appraisal written for you, a homeowner, may not have contained details about the availability of public utilities, a cost to fix flaking paint, a photo and description of the crawlspace, and so on; for some lending purposes, though, these items may be expected by the lender. In some cases, there are specific requirements for legal, tax, and estate appraisals that wouldn’t even be mentioned in other appraisal reports written for other clients.

There are a variety of reasons you might order a private appraisal, so be sure to discuss with the appraiser exactly what it will be used for.

This article was first published from The Daily Sentinel- GJ Real Estate Weekly.

Key Parts of Residential Appraisal Reports Colorado

Not too long ago I was at a school event for my youngest daughter when I started talking to one of the fathers that I knew. During our conversation he mentioned that they were going through the process of refinancing their home and had just received the appraisal back. He shared a little sheepishly that he couldn’t make heads or tails out of it and wondered why the darn thing was so confusing. It reminded me that for someone who doesn’t look at these reports day in and day out they can be a little difficult to understand.

Residential appraisal reports can be quite complex; crammed full with comprehensive market information and different methods for estimating and analyzing value. Sometimes it can be cumbersome to try to sift through all of the information when the average homeowner just wants to get to the bottom line: How much is my home worth?

While the appraisal for a refinance or purchase is used by (and written for) the lender, the document is oftentimes read by the buyers, sellers, and real estate agents. Appraisals are generally performed using similar approaches, regardless of the kind of residential property or which party employs the appraiser (such as for agents or homeowners, for pre-listing appraisals). Appraisers operate in locations they recognize. This provides functioning expertise of any local factors that might influence the value of a property.

The report will include specific attributes of the property and of the surrounding neighborhood. The report will note any damage or recent improvements to the home. There will be maps of the subject property location, as well as the comparable properties’ locations. A perimeter house sketch and pictures of the property are typically included. There will also be pictures of houses that have recently sold in the neighborhood. These are the comparables or “comps”. These recent sales are used to help establish value by analyzing recent sales of similar houses.

A typical appraisal, whether written on a Fannie Mae form for lending or a general purpose form for legal, pre-listing, or other uses, will include the following information:

The Subject: The subject area contains a description of the property including physical street address, legal description, county parcel number, and other identifying information.

The Contract: For a purchase, a summary of the signed purchase contract is provided. Federal regulations require that the lender provide a copy of the contract to the appraiser.

Neighborhood: This section describes characteristics, boundaries, and market conditions of the area and notes the one-unit housing trends. A reader will find information related to increasing, stable, or declining values. In many appraisals, there will also be attachments with further analysis of the market.

Site: The site section of the report covers the physical dimensions of the lot, zoning, nature of the utilities, and flood zone.

Improvements: Sometimes people misunderstand the word “improvements” – it basically means the structure or structures on the property. The lot was improved by putting a house upon it. So the type of house, description, year built, condition, quality, features, square footage, and other characteristics will be detailed in this section.

Sales Comparison Approach: This approach to value is commonly given the most weight in the valuation for residential properties. Here is where I will grid and analyze recent sales of comparable properties in the neighborhood and then make adjustments to the property being appraised. For example, if a comp is bigger than the subject, a negative adjustment may be made; if it is inferior in condition, a positive adjustment may be made. These positive and negative value adjustments are made considering a variety of comparable factors like age, condition, square footage, baths, lot size, and other characteristics that impact marketability and value.

Reconciliation: The sales comparison approach, the cost approach, and/or the income approach (if developed) are reconciled into a final value. If those other two approaches are not used, the final value opinion is established using only the sales comparison approach.

Of course, these are just a few of the key areas of an appraisal report. I always remind people that the appraisal report is an essential document – whatever its intended use is – and a user of the report really needs to take the time to read it, ask questions, and confidently understand it.