Not too long ago I was at a school event for my youngest daughter when I started talking to one of the fathers that I knew. During our conversation he mentioned that they were going through the process of refinancing their home and had just received the appraisal back. He shared a little sheepishly that he couldn’t make heads or tails out of it and wondered why the darn thing was so confusing. It reminded me that for someone who doesn’t look at these reports day in and day out they can be a little difficult to understand.

Residential appraisal reports can be quite complex; crammed full with comprehensive market information and different methods for estimating and analyzing value. Sometimes it can be cumbersome to try to sift through all of the information when the average homeowner just wants to get to the bottom line: How much is my home worth?

While the appraisal for a refinance or purchase is used by (and written for) the lender, the document is oftentimes read by the buyers, sellers, and real estate agents. Appraisals are generally performed using similar approaches, regardless of the kind of residential property or which party employs the appraiser (such as for agents or homeowners, for pre-listing appraisals). Appraisers operate in locations they recognize. This provides functioning expertise of any local factors that might influence the value of a property.

The report will include specific attributes of the property and of the surrounding neighborhood. The report will note any damage or recent improvements to the home. There will be maps of the subject property location, as well as the comparable properties’ locations. A perimeter house sketch and pictures of the property are typically included. There will also be pictures of houses that have recently sold in the neighborhood. These are the comparables or “comps”. These recent sales are used to help establish value by analyzing recent sales of similar houses.

A typical appraisal, whether written on a Fannie Mae form for lending or a general purpose form for legal, pre-listing, or other uses, will include the following information:

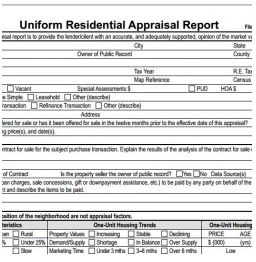

The Subject: The subject area contains a description of the property including physical street address, legal description, county parcel number, and other identifying information.

The Contract: For a purchase, a summary of the signed purchase contract is provided. Federal regulations require that the lender provide a copy of the contract to the appraiser.

Neighborhood: This section describes characteristics, boundaries, and market conditions of the area and notes the one-unit housing trends. A reader will find information related to increasing, stable, or declining values. In many appraisals, there will also be attachments with further analysis of the market.

Site: The site section of the report covers the physical dimensions of the lot, zoning, nature of the utilities, and flood zone.

Improvements: Sometimes people misunderstand the word “improvements” – it basically means the structure or structures on the property. The lot was improved by putting a house upon it. So the type of house, description, year built, condition, quality, features, square footage, and other characteristics will be detailed in this section.

Sales Comparison Approach: This approach to value is commonly given the most weight in the valuation for residential properties. Here is where I will grid and analyze recent sales of comparable properties in the neighborhood and then make adjustments to the property being appraised. For example, if a comp is bigger than the subject, a negative adjustment may be made; if it is inferior in condition, a positive adjustment may be made. These positive and negative value adjustments are made considering a variety of comparable factors like age, condition, square footage, baths, lot size, and other characteristics that impact marketability and value.

Reconciliation: The sales comparison approach, the cost approach, and/or the income approach (if developed) are reconciled into a final value. If those other two approaches are not used, the final value opinion is established using only the sales comparison approach.

Of course, these are just a few of the key areas of an appraisal report. I always remind people that the appraisal report is an essential document – whatever its intended use is – and a user of the report really needs to take the time to read it, ask questions, and confidently understand it.