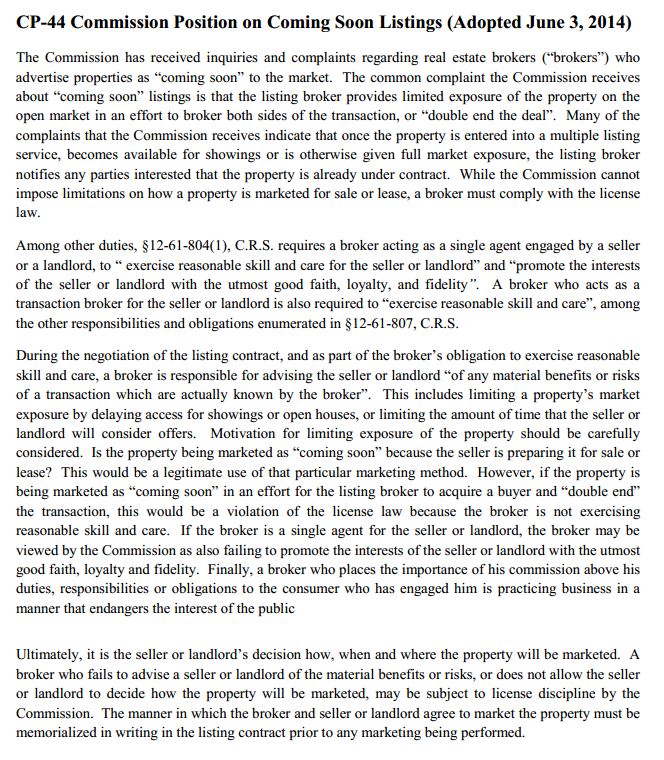

Click the image to read the text of CP-44, Adopted June 3, 2014…  The Colorado Division of Real Estate site is here.

The Colorado Division of Real Estate site is here.

Category: Rules and Regulations

AMC Appraisal Fees and Disclosure- Joshua Walitt

The proposed AMC Rules from the Agencies are out in draft form. Coalitions, industry organizations, and groups of appraisers are examining these and other Rules. There is discussion amongst appraiser groups and other industry participants like never before. It’s a great time to make your voice heard and to hear what others have to say!

When I helped put together a petition to the CFPB a few weeks ago (related to correcting the Customary and Reasonable Fee Rules which allows circumventing the intent of Dodd-Frank), I never imagined the amount of responses I would receive. With so much change going on in the industry, I encourage every appraiser to be involved:

-

What is your Appraiser Coalition doing?

-

How can you be involved in the local chapters of AI and other appraisal organizations?

-

Have you read your State’s Appraiser and AMC rules?

-

Have you read the Appraiser Independence rules established by CFPB, HUD, the Agencies, and other entities?

-

Who do you contact if you have questions regarding State laws and rules?

-

Have you contacted the CFPB regarding enforcement of Appraiser Independence or Customary and Reasonable Fees?

-

Have you completed any and all available fee surveys related to establishing your area’s typical (aka Customary and Reasonable) fees?

-

When was the last time you met with other appraisers in your area?

-

Have you signed and shared the Petition to the CFPB?

-

Are you part of online discussion groups that are positive and share useful information?

Obviously, we all need time to do our work, but issues related to our independence and our fees are part of the foundation of that work itself, so we need to make time to be engaged in the industry discussion. My talk at Valuation Expo this June will touch on related fee issues, with the overall topic being compliance-related issues and their practical applications to our everyday work.

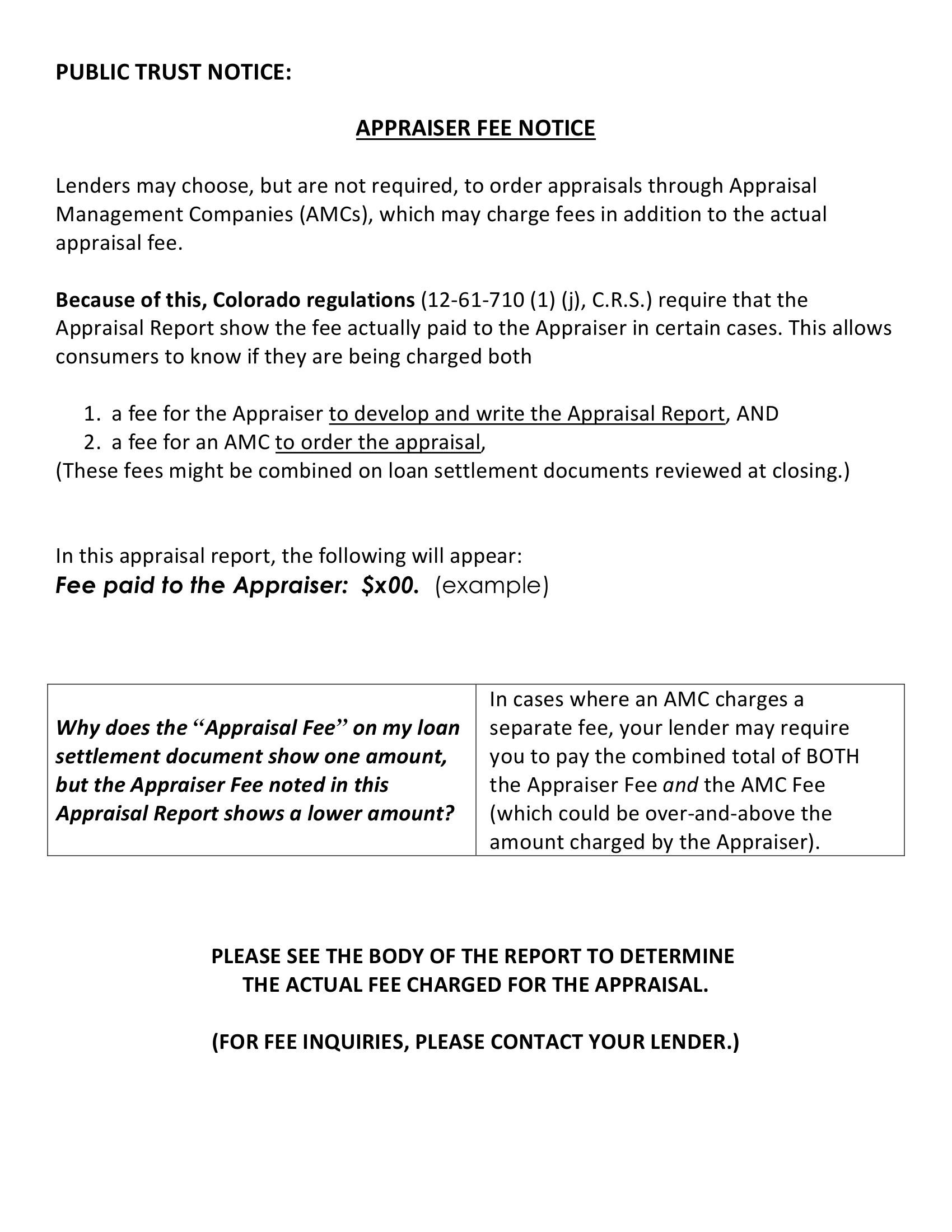

One argument against the Rule-based solution is the assumption that consumers, in the end, really don’t care how much an appraiser is paid. (So is this really a consumer issue? the argument goes.) While consumers may not care about an appraiser’s paycheck per se, let’s not fool ourselves: consumers do care 1) how much they are paying, and 2) what they are paying for. I would argue that consumers DO care how much the appraiser is receiving – since it may differ from what they are charged on the settlement sheet (which may reflect a higher fee than is necessary).

If a loan settlement document shows the consumer is being charged $600 for the Appraisal Fee, I think that consumer would find it surprising – and confusing – to learn the appraiser was actually paid $300 (this is an illustration). Even real estate agents and loan officers tell me they are confused over this issue: Why does the appraisal report say the fee is $300, but the borrower is being charged $600?

The CFPB allows lenders to separate the two fees on the settlement document. But in situations where the lender chooses to comingle the fees on the settlement document, the consumer may not realize they are being required to pay an AMC fee – which is an optional service.

To help alleviate this confusion, many states now require appraisers to post their fees in the reports. HUD also gives this authority to the appraiser for FHA appraisals. (Some AMCs expect the appraiser to post the breakdown of fees within the body of the report.) I have posted my fee in appraisal reports for years.

But be sure to include a disclosure explaining why the Appraisal Fee on settlement documents may differ from the fee you’ve typed in your report, so there is a clear explanation of any “additional” or “different” fees. Take a look at a sample here.

In the end, Appraiser Independence and Fee issues are complex and there is no easy one-route solution. We must proceed with caution.

My two points today:

-

CFPB Rules related to C & R Fees do not allow for any real enforcement of Dodd-Frank, and need correction.

-

Post the Appraiser Fee in the body of the appraisal report with a clear and understandable explanation to avoid consumers misundertanding settlement documents.

Take a look at the Petition, and please sign and share it. But don’t stop there: Know your industry, Get involved, Take action.

Josh Walitt

Originally published at appraisalbuzz.com .

Appraiser Fee Disclosure sample

Here’s the sample Appraiser Fee Disclosure. (Click the image.)

Q & A with Josh Walitt on Residential Appraisals Colorado

Question #1:

Question #1:

My bank said they ordered an appraisal for my loan, but no one ever came inside the house. Does this sound right to you?

For certain types of loans, such as home equity loans, banks follow specific federal guidelines (called Interagency Guidelines) which allow for the bank to use an exterior-only appraisal from a licensed or certified appraiser in some cases. These types of exterior appraisals are typically used in low-risk lending situations, and can also used by banks for pre-foreclosure, loss-mitigation, and similar situations. Since the property is only observed from the street, the homeowner may not even know that the appraiser’s visit took place.

With exterior-only appraisals (sometimes referred to as “drive-bys”), assumptions are made about the interior, sides (if not visible from the street), and rear of the property, as well as the site in general, based on the limited viewing of the property, along with public records, any records in the local real estate MLS system, aerial imagery, or file information the appraiser has on the property, as long as the sources are determined to be reliable. For example, the appraiser may see that the visible parts of the property are in average condition displaying little-to-no needed repairs, so he could assume that the entire property is of similar condition. Or, based on the county records, the appraiser could assume the subject has a covered back patio, a fireplace, and a detached utility building, none of which is visible from the street. Keep in mind, these exterior-only appraisals are not typically ordered for first-mortgage loans, such as when you buy a house.

For first mortgages, a full appraisal is usually conducted, which includes the appraiser viewing the inside and outside of the property. In these situations, the inventory of the property is observed by the appraiser (rather than making assumptions, as in exterior reports). However, it is important to remember that the appraiser is not a home inspector, so he will still make certain assumptions. For example, the appraiser may assume the utilities are functional, the structure is sound, there are no health hazards, and so on, as long as there is no evidence to the contrary.

There are some situations where the bank can loan without the use of an appraisal. If there is ever any question, remember this: a borrower can ask to review copies of all valuation reports that the lender used.

Question #2:

I got my own appraisal a few months ago because I was thinking of listing my house for sale. Now I want to refinance, but my banker won’t take that appraisal.

There are several factors at work here.

First, banks are required to order their own appraisals, ensuring certain Appraiser Independence regulations are met. For a privately ordered appraisal, such as for a legal matter, a trust, an estate following a death, or a pre-listing appraisal, these regulatory safeguards are most likely not met. Banks and lenders have internal departments and staff that carry out and monitor the appraisal-ordering procedures, although some choose to use third parties.

Second, an appraisal has specified Intended Use and Intended Users. To follow federal rule, appraisers must identify the Use and Users of an appraisal report. Examples include: to determine a property’s market value to aid in listing it for sale by the homeowner and real estate agent, to determine market value for divorce purposes by Mr. Smith and his attorney, and so on. The Use and User for lending appraisals may often be to evaluate the property for mortgage purposes by the lender.

Why is this so important? The Use can impact what the appraiser is trying to solve: is it liquidation value, market value, a range of values, before- and after- remodel values, a future anticipated sale price? And the Intended User can be a very important factor in the level of detail and information that the appraiser provides in his report. For example, writing for a lender, the appraiser would not hesitate to use terms such as “bracketing”, “highest-and-best use”, “super-adequacy”, “regression analysis”, and so on; these terms could confuse many homeowners, agents, or attorneys, unless there was further explanation in the report. Consider that the appraisal written for you, a homeowner, may not have contained details about the availability of public utilities, a cost to fix flaking paint, a photo and description of the crawlspace, and so on; for some lending purposes, though, these items may be expected by the lender. In some cases, there are specific requirements for legal, tax, and estate appraisals that wouldn’t even be mentioned in other appraisal reports written for other clients.

There are a variety of reasons you might order a private appraisal, so be sure to discuss with the appraiser exactly what it will be used for.

This article was first published from The Daily Sentinel- GJ Real Estate Weekly.

Agencies Issue Proposed Rule on Minimum Requirements for Appraisal Management Companies

Six agencies released a Joint Release “Agencies Issue Proposed Rule on Minimum Requirements for Appraisal Management Companies”. The release, and its attached Proposed Rule, list five AMC requirements that participating States must enforce, as well as six broad powers the States must have related to monitoring, disciplining, and reporting.

The Joint Release also points out to States that participation is not mandatory; non-participation by a State would bar appraisal management companies from doing business in that State related to federally-related transactions.

Read the Joint Release and the Proposed Rule. The Proposed Rule contains instructions for comment.

———————————————————————————————————————-

WASHINGTON— Six agencies today issued a proposed rule that would implement minimum requirements for state registration and supervision of appraisal management companies (AMCs). An AMC is an entity that serves as an intermediary between appraisers and lenders and provides appraisal management services.

In accordance with section 1124 of Title XI of the Financial Institution Reform, Recovery, and Enforcement Act of 1989, as added by section 1473 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, the minimum requirements in the proposed rule would apply to states that elect to establish an appraiser certifying and licensing agency with the authority to register and supervise AMCs.

The proposed rule would not compel a state to establish an AMC registration and supervision program, and there is no penalty imposed on a state that does not establish a regulatory structure for AMCs. However, an AMC is barred by section 1124 from providing appraisal management services for federally related transactions in a state that has not established such a regulatory structure.

Under the proposed rule, participating states would require that an AMC:

Register in the state and be subject to its supervision;

Use only state-certified or licensed appraisers for federally related transactions, such as real estate-related financial transactions overseen by a federal financial institution regulatory agency that require appraiser services;

Require that appraisals comply with the Uniform Standards of Professional Appraisal Practice;

Ensure selection of a competent and independent appraiser; and

Establish and comply with processes and controls reasonably designed to ensure that appraisals comply with the appraisal independence standards established under the Truth in Lending Act.

The proposed rule also would require that the certifying and licensing agency of a participating state have certain authorities, including the authority to:

Approve or deny initial AMC registration applications and applications for renewals;

Examine the AMC and require the AMC to submit relevant information to the state;

Verify that the appraisers on the AMC’s appraiser network or panel hold valid state certifications or licenses;

Conduct investigations of AMCs to assess potential violations of appraisal-related laws;

Discipline an AMC that violates appraisal-related laws; and

Report an AMC’s violation of appraisal-related laws, as well as disciplinary and enforcement actions, and other pertinent information about an AMC’s operations to the Appraisal Subcommittee of the Federal Financial Institutions Examination Council.

The proposed rule would provide participating states 36 months after its effective date to implement the minimum requirements. An AMC that is a subsidiary of a financial institution and regulated by a federal financial institution regulatory agency is required by section 1124 and the proposed rule to meet the same minimum requirements as other AMCs, although such an AMC is not required to register with a state.

In conjunction with the proposal, the Federal Deposit Insurance Corporation is proposing to rescind appraisal regulations promulgated by the former Office of Thrift Supervision (OTS). The OTS appraisal regulations are duplicative of the FDIC’s appraisal regulations in Part 323. Similarly, in a separate rulemaking, the Office of the Comptroller of the Currency is rescinding appraisal regulations promulgated by the former OTS.

The proposal is being issued jointly by the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the Consumer Financial Protection Bureau, the Federal Housing Finance Agency, and the National Credit Union Administration.

The Federal Register notice is attached. The agencies are seeking comments from the public on all aspects of the proposal. The public will have 60 days to review and comment on the proposal and the proposed Paperwork Reduction Act analysis. Publication of the proposal in the Federal Register is expected shortly.

Attachment: Minimum Requirements for Appraisal Management Companies – PDF

Media Contacts:

OCC Stephanie Collins (202) 649-6870

Federal Reserve Susan Stawick (202) 452-2955

FDIC Greg Hernandez (202) 898-6984

CFPB Sam Gilford (202) 435-7673

FHFA Corinne Russell (202) 649-3032

NCUA Ben Hardaway (703) 518-6333

PR-21-2014